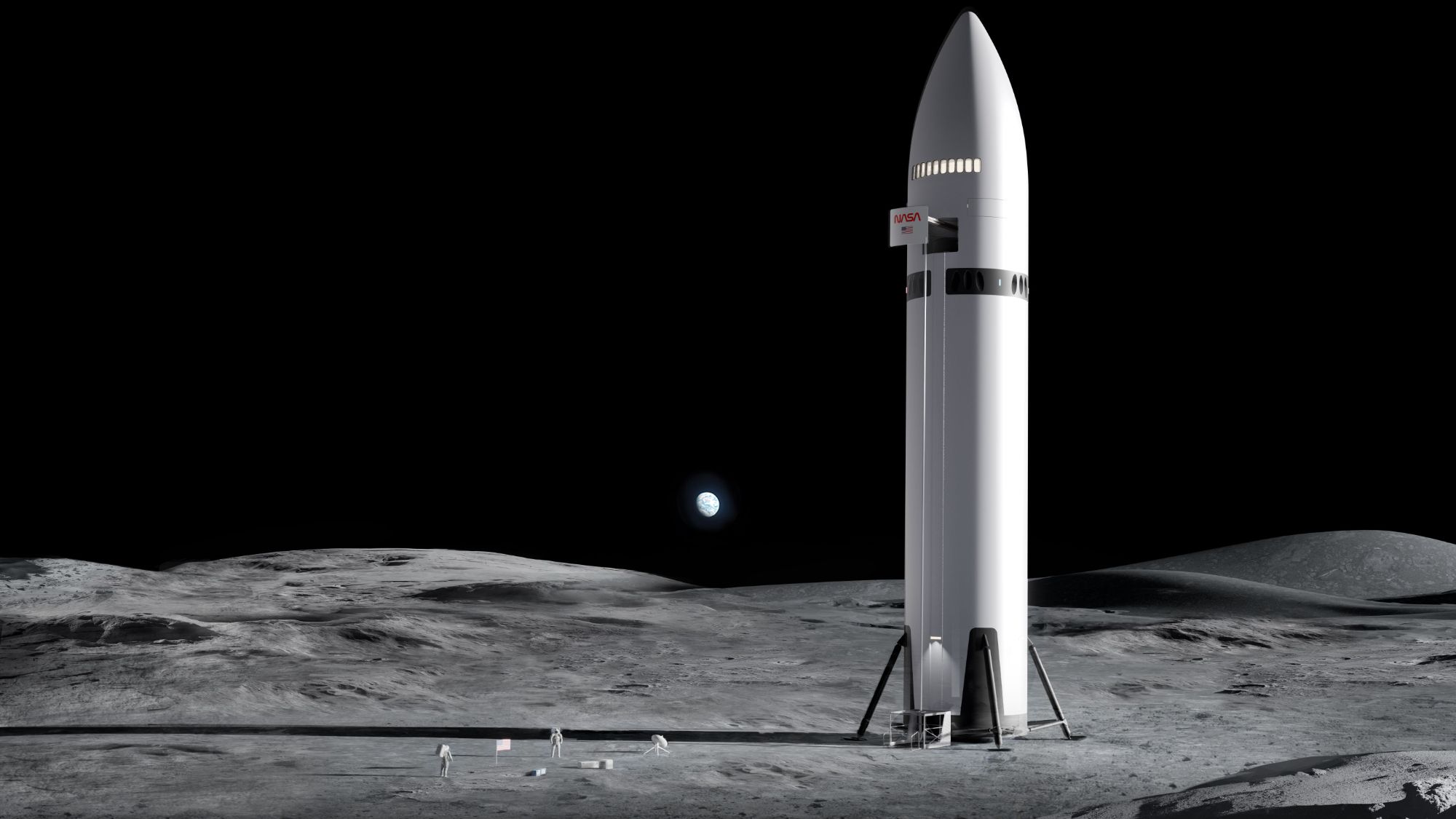

NASA has restructured its Artemis architecture, removing a lunar landing from Artemis 3 and refocusing that mission as a 2027 low-Earth-orbit demonstration of rendezvous and docking between Orion and one or both commercial landers from SpaceX and Blue Origin. The first crewed lunar landing is now targeted for Artemis 4 in 2028 (with Artemis 5 possibly the same year), while NASA plans to retain the SLS Block I configuration and deliberately foster competition between contractors—citing development pace and the desire to avoid reliance on a single provider; Blue Origin has paused suborbital tourism to accelerate lunar lander work and SpaceX’s Starship has yet to reach orbit despite recent successful tests.

Market structure: NASA’s move to keep Artemis 3 in LEO and reopen competition shifts near-term revenue from a single private supplier (SpaceX) back toward diversified primes and NASA contractors. Expect incumbents tied to SLS and LEO rendezvous infrastructure (Aerojet Rocketdyne, Lockheed, Northrop, prime contractors) to see steadier contract pipelines over 12–36 months; commercial-only landers face elongated monetization timelines by 1–3 years. Risk assessment: Tail risks include a rapid Starship orbital certification (weeks–months) that would re-concentrate launch/landing economics toward SpaceX, and congressional budget cuts (≥20% to Artemis line items) that would materially reduce contractor cash flow. Hidden dependencies: NASA procurement cadence, GAO/DoD oversight, and port/infrastructure buildout; any one can delay awards by 6–18 months. Key catalysts to watch in the next 30–90 days: Artemis 2 flight, SpaceX orbital tests, and NASA procurement announcements. Trade implications: Favor defensive, cash-flowing aerospace/defense names and ETFs for 6–24 months while avoiding or shorting high‑beta commercial-space pure plays. Use 9–24 month LEAPS on engine/prime suppliers to capture multi-year program awards and sell near-term calls around Artemis 2 to collect premium. Size positions modestly given political/budget uncertainty: 1–3% of portfolio per idea, re-evaluate after the next NASA procurement decision and Artemis 2. Contrarian angles: Consensus frames this as a win for competition; contrarian risk is that standardizing on SLS Block I reduces long-run upside for diversified primes if Congress pivots to a single commercial winner — an event that would compress margins for smaller contractors. Historical parallel: 2000s DoD program consolidations where single-vendor wins produced 30–50% drawdowns in small suppliers; avoid overpaying for small-cap space names on narrative alone.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

0.00

Ticker Sentiment